The Next Squeeze in Bitcoin Mining Isn’t Power. It’s Silicon.

What TSMC's capacity crunch means for Bitcoin mining hardware

Bitcoin miners already felt the pressure of AI and HPC demand in power markets. Now the next constraint is emerging one layer deeper in the stack, at the foundry level According to TSMC supply chain reports cited by DIGITIMES Asia, leading-edge capacity (3nm and below) is under heavy pressure from hyperscalers and AI leaders like Apple and NVIDIA. Bitcoin ASIC manufacturers are now competing for wafer allocation in one of the most capacity-constrained industries globally. And unlike power markets, this isn’t something you can hedge, reroute, or replicate easily.

The Foundry Squeeze

Which OEMs Are Most Exposed

What 2021 Told Us

This Time it’s Different

The Challenge for OEMs to Switch Foundries

Efficiency Gains May Slow

Auradine’s Strategic Pivot and Rebranded to Velaura AI

Will Others Follow Auradine Into AI? - Premium Insights

OEM Winners and Losers in a Constrained Foundry Market - Premium Insights

The Best Miners May Look Different - Premium Insights

Every infrastructure deal follows the same sequence: evaluate, structure, deploy, operate, scale. At each stage, capital can win or break. Most advisors only see part of the picture. Digital Mining Solutions sits across all five by bringing the expertise, relationships, and narrative that turn a single site into a scalable platform.

Deploying capital into digital infrastructure or looking to scale your operations? Hit reply and tell us where you are in the cycle.

The Foundry Squeeze

Bitcoin miners already know what it feels like to be outbid for power. AI/HPC operators arrived with deeper pockets, longer-term contracts, and stronger political backing. The result is visible in how U.S. hashrate growth has slowed and how some of the largest mining companies have quietly pivoted their infrastructure toward compute leasing.

The next version of that story may be playing out upstream at the foundry level. According to a recent report from DIGITIMES Asia, TSMC’s 3nm capacity is under significant pressure from Apple, NVIDIA, and other high-volume customers.

Training clusters scaling into tens of thousands of GPUs, inference workloads requiring constant hardware refresh cycles and hyperscalers locking in multi-year wafer agreements. Capacity is not just scarce; it is pre-allocated. Buyers are not just large, but they have long-term foundry relationships, multi-year volume commitments, and the leverage to secure priority access.

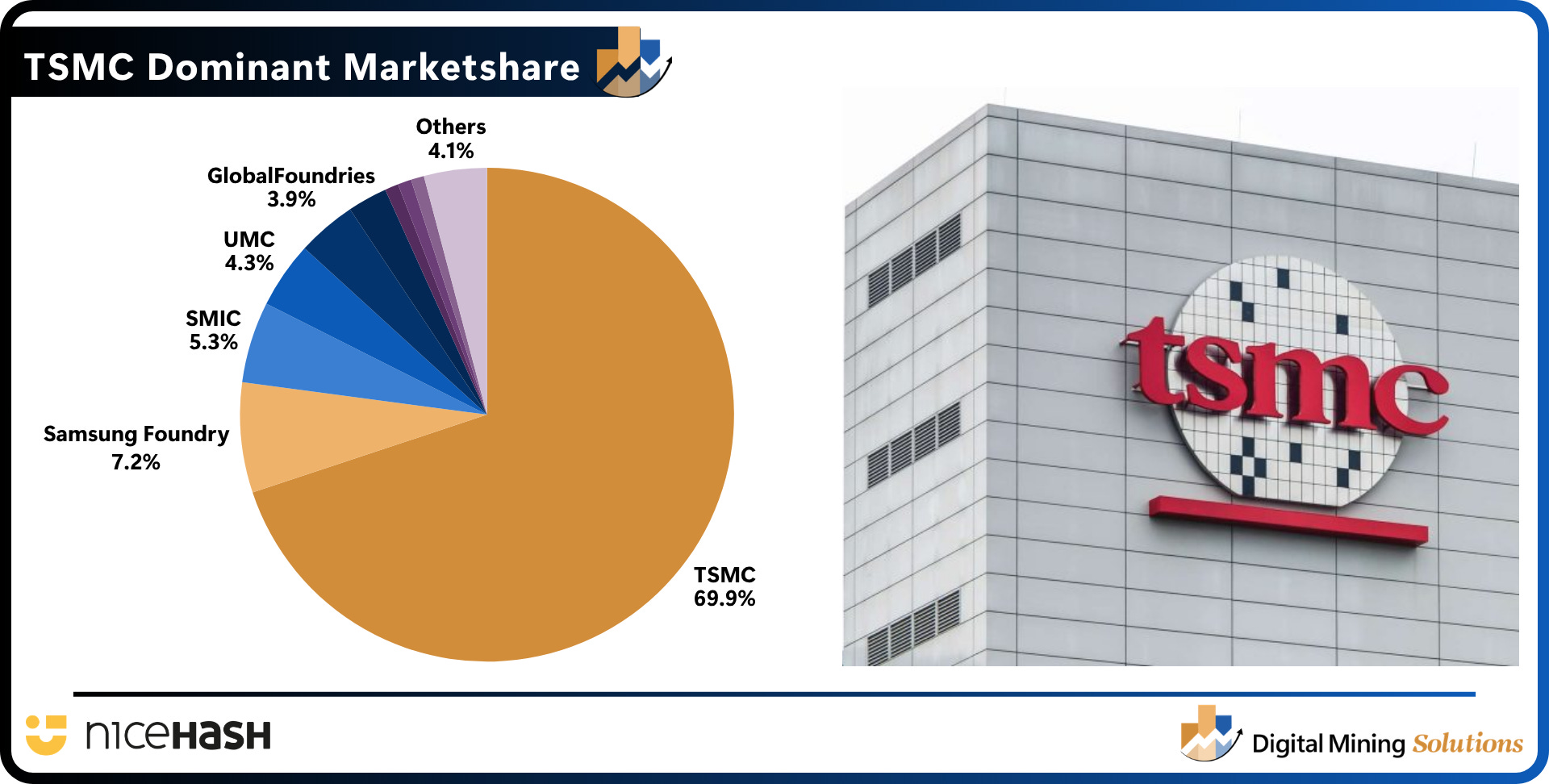

In 2025 TSMC controlled roughly 70% of the global pure-play foundry market, up from the mid-60s just a year earlier. At advanced nodes (5nm, 4nm, 3nm), that dominance is even more pronounced. That concentration matters. When access to leading-edge chips tightens, it tightens inside a market where one foundry largely sets the terms.

Which OEMs Are Most Exposed to TSMC?

Not every ASIC manufacturer is equally affected. But the exposure map inside Bitcoin mining is significant. Bitmain, which commands the largest share of global ASIC production, has built its chip lineage on TSMC. The Antminer S21 series runs on TSMC’s 5nm node. Future roadmap products targeting sub-10 J/TH efficiency are expected to remain on TSMC’s advanced capacity. For Bitmain, there is no obvious alternative, its manufacturing relationships have been built around a single foundry for years.

Bitdeer is also heavily exposed. Its SEALMINER lineup uses TSMC’s 4nm process, and the company’s ambitious roadmap with the recent launch of the fourth-generation SEALMINER, depends on access to TSMC’s most advanced nodes. If wafer allocations get squeezed, this can lead to longer lead times for wafers and less flexibility for design iterations.

MicroBT has historically diversified across multiple foundries, including Samsung. That gives it more flexibility but there’s a trade-off. Samsung currently still lags TSMC at advanced nodes in both yield and performance. That limits how far MicroBT can push next-generation efficiency without compromising on its roadmap. Canaan has taken a similar approach. As the smallest of the major OEMs by market share, it is also the most exposed to execution risk at the foundry level.

The market has already split along foundry lines, with Bitmain and Bitdeer tied to TSMC and MicroBT and Canaan committed to Samsung. The question now is whether Samsung can deliver at the level the hardware roadmaps require.

What 2021 Told Us

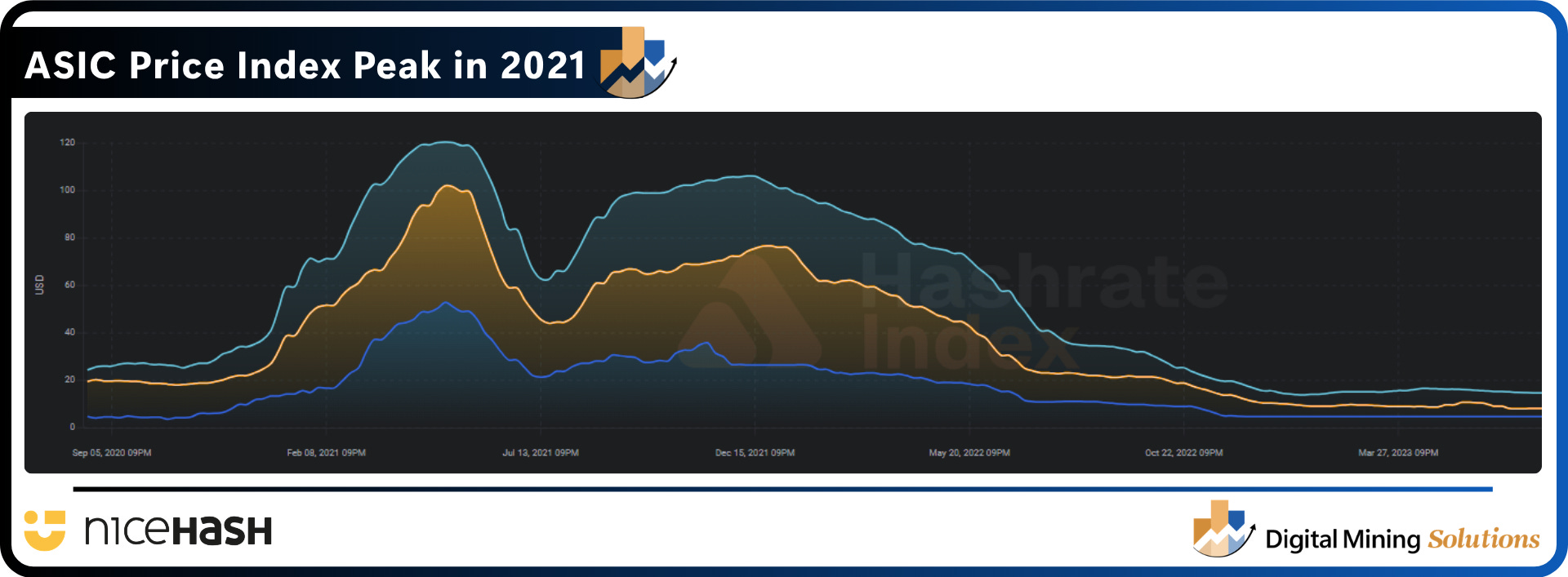

This is not the first time semiconductor supply disruption has hit the Bitcoin mining hardware market. The COVID-era chip shortage of 2021 provides the clearest precedent.

During that period, a global shortage of semiconductor components coincided with one of Bitcoin’s strongest bull runs. The result was a hardware market that seized up quickly. Next-generation ASIC prices surged from roughly ~$30/TH at launch to $80–100/TH or higher within months. Lead times stretched from weeks to six months or more. Miners who had secured forward orders or established OEM relationships held a structural advantage. Those relying on spot availability found themselves priced out or delayed.

The 2021 disruption was demand-led. A rising Bitcoin price attracted new miners, hardware manufacturers couldn’t keep up, and the shortage became self-reinforcing. But the supply chain weakness was the accelerant, it turned a demand spike into a multi-quarter bottleneck.

This Time it’s Different

There are meaningful differences between 2021 and today, and they matter. The most obvious is hashprice. It currently sits near historic lows, well below $40/PH/day. In 2021, miners were expanding into a bull market with strong margins. That year hashprice was swinging between $200 to over $400/TH/day. Today, many operators are deferring capital expenditure rather than accelerating it. That dampens hardware demand and reduces the near-term urgency of a supply squeeze.

But the timing mismatch is the key risk. Foundry lead times are long. If OEMs are unable to secure adequate wafer allocations over the next six to twelve months, the machines that reach market in 2026 might reflect today’s supply constraints, not today’s weak demand environment. If Bitcoin price recovers and hashprice improves, demand for next-generation hardware will accelerate precisely when supply is still catching up. That is the same sequence as 2021, just playing out over a longer timeframe, and likely with less volatility due to a dampened hashprice.

The Challenge for OEMs to Switch Foundries

The natural response to foundry pressure is to diversify. In practice, switching foundries is one of the most expensive decisions an ASIC manufacturer can make.

Each foundry operates with different process design kits, different IP libraries, and different manufacturing rules. A chip designed for TSMC’s 5nm node cannot simply be re-taped out on Samsung’s equivalent without significant re-engineering. That typically takes twelve to eighteen months, sometimes longer, and introduces meaningful risk around yield and performance.

Samsung remains the most realistic alternative, and some OEMs already use it for certain product lines. But Samsung’s advanced node capabilities are not equivalent to TSMC’s at the leading edge. Manufacturers that move designs there may accept efficiency trade-offs that show up directly in J/TH performance, exactly the metric that determines whether a machine is profitable or not.

Efficiency Gains May Slow

One potential consequence of foundry pressure is what it does to the hardware efficiency improvement curve.

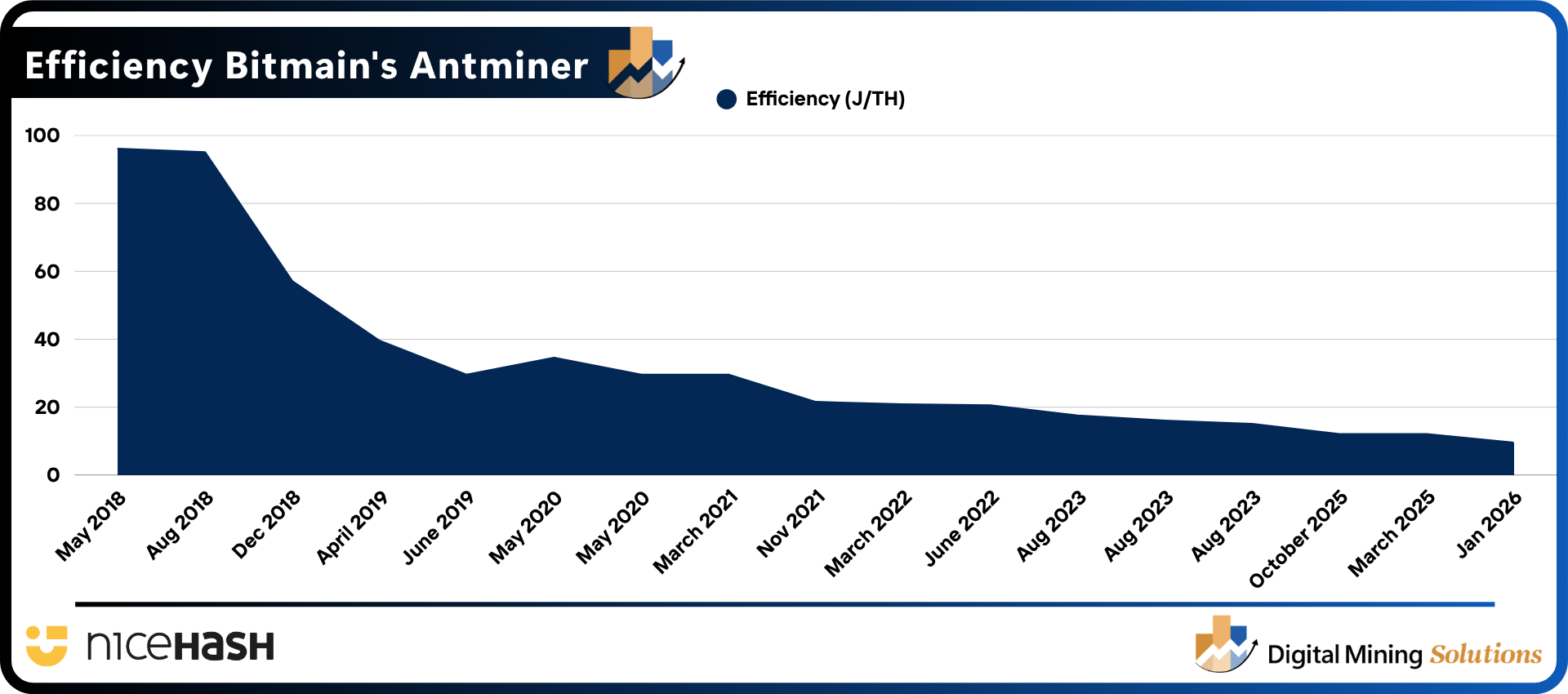

Bitcoin ASIC efficiency has followed a consistent trajectory over the past five years. Each new node generation has delivered meaningful J/TH reductions from 30+ J/TH at 7nm, to mid-teens at 5nm, toward single-digit targets at 4nm. That progression has driven relentless fleet turnover, compressed economic life of older machines and forced miners into increasingly aggressive capex cycles.

If OEMs are delayed onto less advanced nodes or forced to launch on Samsung rather than TSMC’s leading edge, that improvement curve flattens even faster than it already has. The gap between generations narrows. A machine launched on a constrained 5nm process may not deliver the efficiency step-change that would otherwise justify replacing existing 5nm fleets.

That might lead to hardware obsolescence slows down. Older machines stay economically viable longer when the next generation offers only marginal efficiency gains rather than a step-change. The pressure to replace a 19 J/TH fleet diminishes significantly if the best available replacement is 16 J/TH rather than 10 J/TH. Capex cycles become less aggressive, which in a compressed margin environment is not necessarily unwelcome.

The machines that looked like liabilities at the start of this bear market may hold their value longer than expected, not because the market improved, but because the next generation arrived late and underwhelmed. The efficiency race does not stop. But it may slow down enough to change the calculus on when, and how aggressively, to upgrade.

Auradine’s Strategic Pivot and Rebranded to Velaura AI

Auradine’s recent strategic pivot deserves attention in this context. Even if the primary reason was not driven by its foundry strategy.

The company has rebranded as Velaura and pivoted its core focus from Bitcoin ASIC production to AI compute silicon. The company focuses on a structural bottleneck in AI scaling, energy consumption rather than raw compute performance. Its new Titan Core platform is a silicon design and IP stack that claims up to 50% reductions in chip power consumption for AI accelerators, with 2–4x efficiency gains at the circuit level on matrix multiplication workloads. The company says that translates into up to 500 watts of power savings per chip and is already working with hyperscalers and chip partners at 3nm and 2nm nodes.

That is a credible technical story. But reading between the lines, the timing is hard to separate from conditions in the mining market. Auradine gained genuine traction as a domestic alternative in Bitcoin hardware. Its Teraflux series launched with efficiencies comparable to Bitmain’s leading products, which was a meaningful achievement for a newer entrant. But the prolonged collapse in hashprice has lowered new ASIC demand across the industry. Even Bitmain and MicroBT have been managing excess inventory. For a smaller, VC-backed manufacturer without the order book depth of the incumbents, that environment is existential. The pivot was almost certainly shaped as much by what was happening in mining as by what is happening in AI.

A manufacturer that can present a credible AI silicon roadmap to a foundry, at 3nm and 2nm, with hyperscaler partnerships and an energy efficiency story that aligns with where AI infrastructure is heading, is a fundamentally different kind of customer than a pure Bitcoin ASIC maker. It offers volume visibility, margin stability, and strategic alignment with TSMC’s most important growth segment. In a constrained foundry environment, that profile earns a different level of priority. The pivot may have been driven by necessity but the strategic upside is real regardless.

The premium section below breaks down which OEMs are most and least exposed to TSMC constraints, what a realistic worst-case looks like for hardware timelines, and whether Auradine’s AI pivot is a one-off or the early signal of a broader shift in how ASIC manufacturers think about their foundry relationships.

If you found this useful, forward it to someone running a mining operation or evaluating hardware capex this year.

Leverage data-driven insights and a powerful network to launch strong, optimize efficiently, and scale with confidence. We offer:

Market Intelligence - Masterclasses, Tailored Reports & Articles and Industry Benchmarks.

Advisory Services - Business Plan Assessment, Investor Presentations, M&A Advisory and Executive Coaching.

Sites & Rackspace - Due Diligence & Partnership Matchmaking, Institutional Investment Guidance and Rackspace Sales

Elevate your mining operation today with Digital Mining Solutions!

If you enjoy the content, if you have not subscribed, please ensure to click the button below and share The Bitcoin Mining Block Post.

If you want to stay ahead in the world of Bitcoin mining, make sure to follow me on Twitter and LinkedIn. Would you like to become a sponsor of the newsletter or are you interested in a workshop on mining economics? Contact me at nicosmid@digitalminingsolutions.tech.